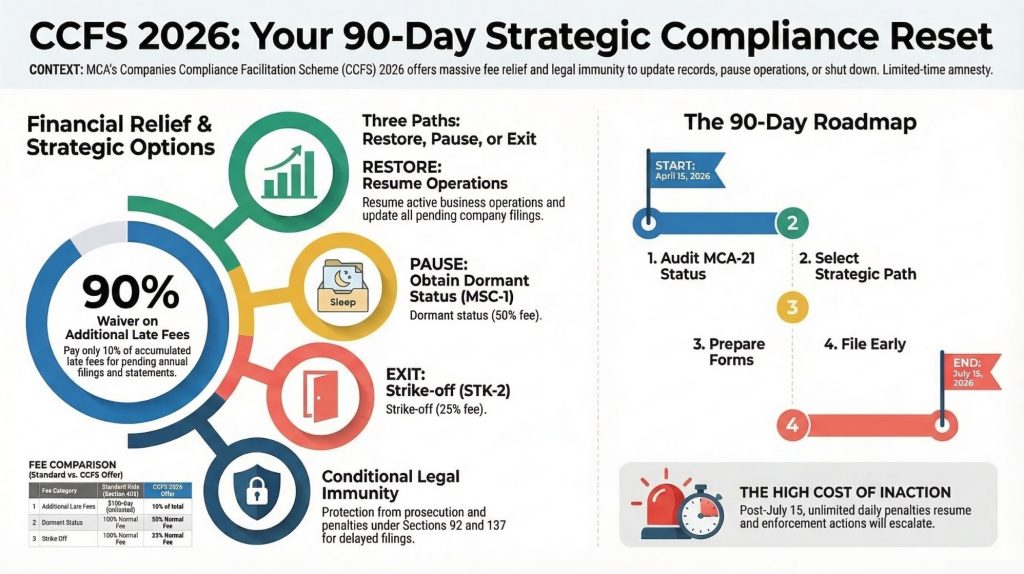

The Ministry of Corporate Affairs has introduced a new scheme named the Companies Compliance Facilitation Scheme, 2026 (CCFS 2026). This is a one-time opportunity to clear their pending ROC filings at a substantially reduced cost.

This scheme will remain available from 15 April 2026 to 15 July 2026. During this period, the companies can file the overdue annual returns and financial statements by paying 10% of the additional late fees along with the normal filing charges.

For many companies, this is a practical chance to clean up their MCA records, reduce potential penalties and take a call on the future of the company of whether to continue, pause or close it altogether.

What Does the Scheme Offer?

CCFS 2026 gives companies three clear options depending on their situation:

- Catch up on pending filings

If filings have been missed over the years, they can now be completed with a 90% waiver on late fees. This can save a fortune where delays have accumulated. - Keep the company but reduce compliance

Where the business is not active, apply for dormant status (MSC-1) at half the usual fee. This helps reduce ongoing compliance without closing the entity. - Close the company in a simpler way

If the company wants to shut down, apply for strike-off (STK-2) by paying only 25% of the standard fee, making it a relatively cost-effective exit.

The scheme also provides immunity from penalties and prosecution related to delays, provided the filings are completed within the prescribed timelines.

Key Forms Covered

The scheme focuses on routine annual filings and related forms under both the Companies Act, 2013 and earlier 1956 Act.

| Category | Main Forms Included |

| Annual returns | MGT‑7, MGT‑7A, Form 20B, Form 21A |

| Financial statements | AOC‑4, AOC‑4 CFS, AOC‑4 (XBRL), 23AC, 23ACA, 23AC‑XBRL, 23ACA‑XBRL |

| Auditor‑related | ADT‑1, Form 23B, Form 66 (compliance certificate) |

| Foreign companies | FC‑3, FC‑4 |

| Status‑change forms (fee concessions) | MSC‑1 (dormant status), STK‑2 (strike‑off) |

If filings are pending for multiple years, the overall cost savings under this scheme can be quite substantial.

Who Should Seriously Consider CCFS‑2026?

This scheme is primarily relevant for:

- Companies with several years of pending filings where late fees have piled up

- Businesses that are inactive but want to keep the company alive with minimal compliance.

- Companies that are no longer operating and would prefer to close down rather than carry ongoing legal risk

Who cannot use the scheme?

Companies not eligible include:

- Companies already under a final strike-off notice under section 248

- Companies that have already applied for strike-off or dormant status before this scheme

- Companies dissolved through amalgamation

- Vanishing companies as defined by the regulations

Practical Steps for Companies

Take the benefit of this 90 day window by following three simple steps:

- Review MCA status

Check all filings that are pending across all financial years. - Decide the direction

Based on current plans, choose to continuing, go dormant or close the company. - Act early

Prepare the financials and complete the filings well before the deadline to avoid last minute issues or portal delays.

Schemes like this don’t come often with a period of 90-day. The goal could be to regularise, pause operations, or exit. But the key is to take a timely decision rather than letting the compliances pile up. A structured approach now can save one, both time and cost later. But more importantly, it will help avoid avoidable regulatory exposure.